Perovskite-silicon tandem solar cells have finally broken through from laboratory prototypes to commercial production, with record efficiencies exceeding 34 percent and the first factory-scale modules shipping worldwide. For Indian buyers, this next-generation technology promises more power from the same roof space, but practical adoption depends on stability improvements, cost competitiveness, and supply chain maturity.

The Tandem Technology Breakthrough

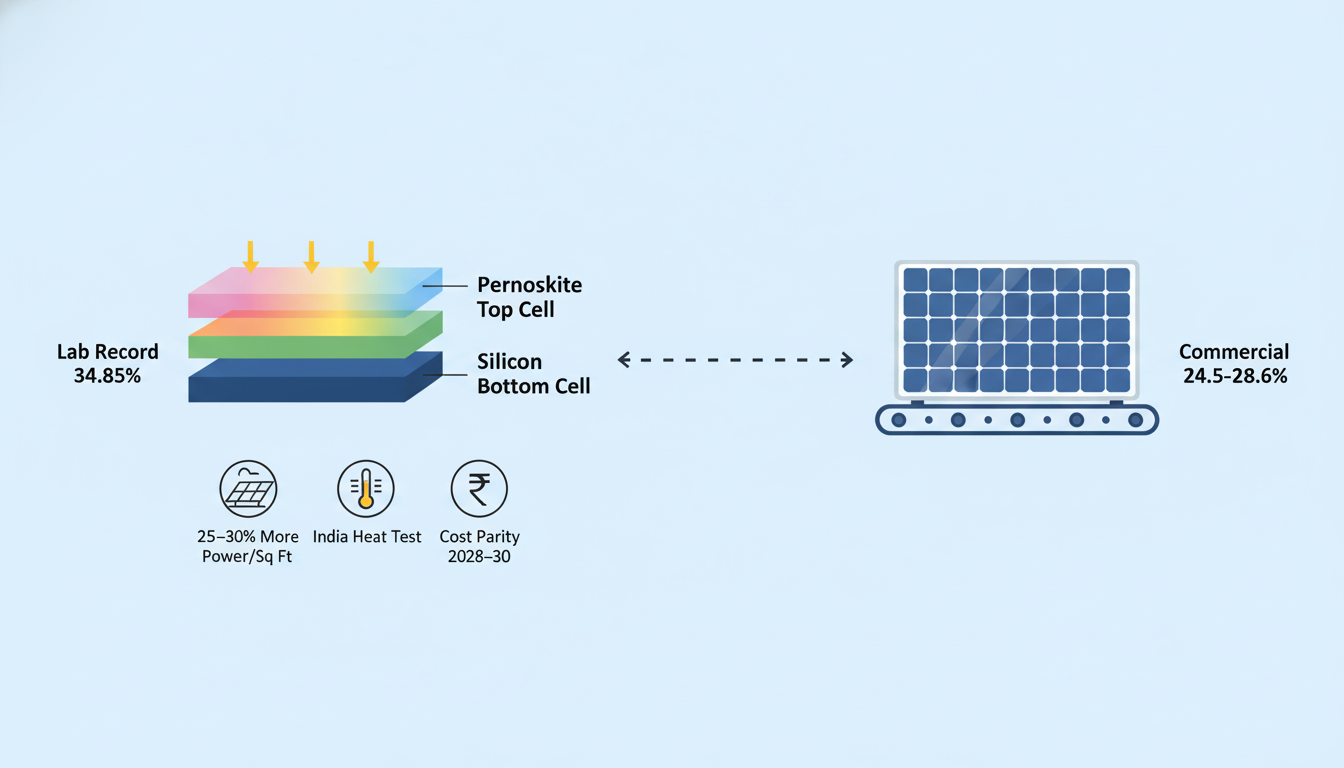

Tandem solar cells stack a thin-film perovskite layer on top of traditional silicon cells, capturing different parts of the sunlight spectrum for higher overall efficiency. In late 2025, LONGi achieved a certified 34.85 percent efficiency for a two-terminal perovskite-silicon tandem cell, smashing the 33.7 percent theoretical limit of single-junction silicon cells. Oxford PV shipped the world's first commercial-sized tandem modules at 24.5–28.6 percent efficiency from their German production line, proving the technology can scale beyond lab samples.

These efficiencies mean a tandem module generates roughly 25–30 percent more electricity than conventional silicon panels of the same size, directly translating to more savings from smaller rooftops or more revenue from ground-mounted projects.

Commercial Milestones and Global Leaders

Oxford PV's Brandenburg facility—operational since 2017—now produces volume tandem modules, marking the first industrial-scale deployment of perovskite technology. Sharp announced plans for mass production of lightweight perovskite-silicon tandems by fiscal 2027, leveraging OLED manufacturing experience to cut costs by 10 percent. JinkoSolar and other Chinese giants are scaling pilot lines, while Indian institutions like IIT Bombay developed a 30.2 percent efficient transparent 4T tandem cell, positioning India as a research leader.

Global pilots target niche applications first: building-integrated photovoltaics (BIPV), lightweight panels for electric vehicles, portable power, and space-constrained commercial rooftops where higher efficiency per square foot justifies premium pricing.

Stability and Durability: The Remaining Hurdles

Perovskite's Achilles heel has been stability—early cells degraded rapidly from moisture, heat, UV exposure, and ion migration. Commercial tandems now use encapsulation techniques, passivation layers, and composition engineering to achieve 1,000+ hour stability under accelerated stress tests equivalent to 20–25 years in the field. Oxford PV's modules meet IEC standards for commercial viability, and LONGi's record cells show improved thermal cycling and damp-heat resistance.

For India, where panels face extreme heat (50°C+), dust, monsoon humidity, and pollution, long-term outdoor stability remains the key question. Indian research emphasizes wide-bandgap perovskites optimized for hot climates, addressing degradation that hits harder in tropical conditions.

Cost Trajectory and Market Entry

Early commercial tandems carry a premium—estimated 20–30 percent above standard silicon—but falling perovskite material costs (iodine, lead, organic halides) and shared silicon production lines will narrow the gap. Analysts project tandems reaching cost parity with high-efficiency silicon (22–24 percent) by 2028–2030 as volumes scale. Initial Indian pricing will likely target premium segments: commercial rooftops, EV charging stations, and government pilot projects under PLI schemes promoting advanced PV manufacturing.

What It Means for Indian Buyers in 2026

Residential buyers won't see tandems on rooftops immediately—limited availability and higher upfront costs mean standard silicon remains dominant for homes. Early adopters may find BIPV options for modern villas or apartments, but widespread residential availability likely starts 2027+.

Commercial and industrial buyers gain the most: 25–30 percent more output from the same roof space translates directly to higher savings, especially for high-tariff businesses in Delhi-NCR and UP. Niche applications like agrivoltaics, EV infrastructure, and floating solar could deploy tandems sooner.

Policy and manufacturing opportunities abound: India's PLI scheme and ALMM framework encourage domestic tandem production, with IITs and startups positioning for early-mover advantage. By 2026, limited imports from Oxford PV, LONGi, or Sharp will test market reception, paving the way for local giga-factories.

Challenges and Realistic Expectations

Commercial tandems aren't a "drop-in" replacement. Supply chains for perovskite precursors are nascent, recycling protocols are undeveloped, and long-term field data (10+ years) is absent. Indian buyers should demand IEC certifications, third-party warranties, and performance guarantees before committing.

For 2026, expect selective availability in premium projects rather than mass-market rooftops. The real value lies in proving reliability under Indian conditions—heat, dust, humidity—before scaling to utility parks and exports.

FAQs

Q1. Are perovskite-silicon tandem cells commercially available in India in 2026?

A1. Limited commercial availability exists in 2026 for premium projects, but mass-market residential adoption likely starts 2027+ as stability and supply chains mature.

Q2. What efficiency do commercial tandem cells achieve?

A2. Commercial modules from Oxford PV achieve 24.5–28.6 percent efficiency, with lab records at 34.85 percent from LONGi.

Q3. Who should buy tandems first in India?

A3. Commercial rooftops, EV charging, BIPV, and agrivoltaics benefit most from higher output per square foot in space-constrained applications.

Q4. Are tandems stable enough for India's climate?

A4. Improved encapsulation and passivation achieve 20–25 year field-equivalent stability, but long-term tropical data is still emerging.

Q5. Will tandems qualify for PM Surya Ghar subsidies?

A5. MNRE subsidies apply to ALMM-certified modules; tandems may qualify once domestically produced and certified under PLI schemes.