India is projected to overtake the United States in 2026 to become the world’s second‑largest solar market, behind only China. BloombergNEF estimates India will add just over 50 GW of new solar capacity in 2026, even as global installations dip due to a slowdown in China’s growth.

What the 50+ GW Milestone Means

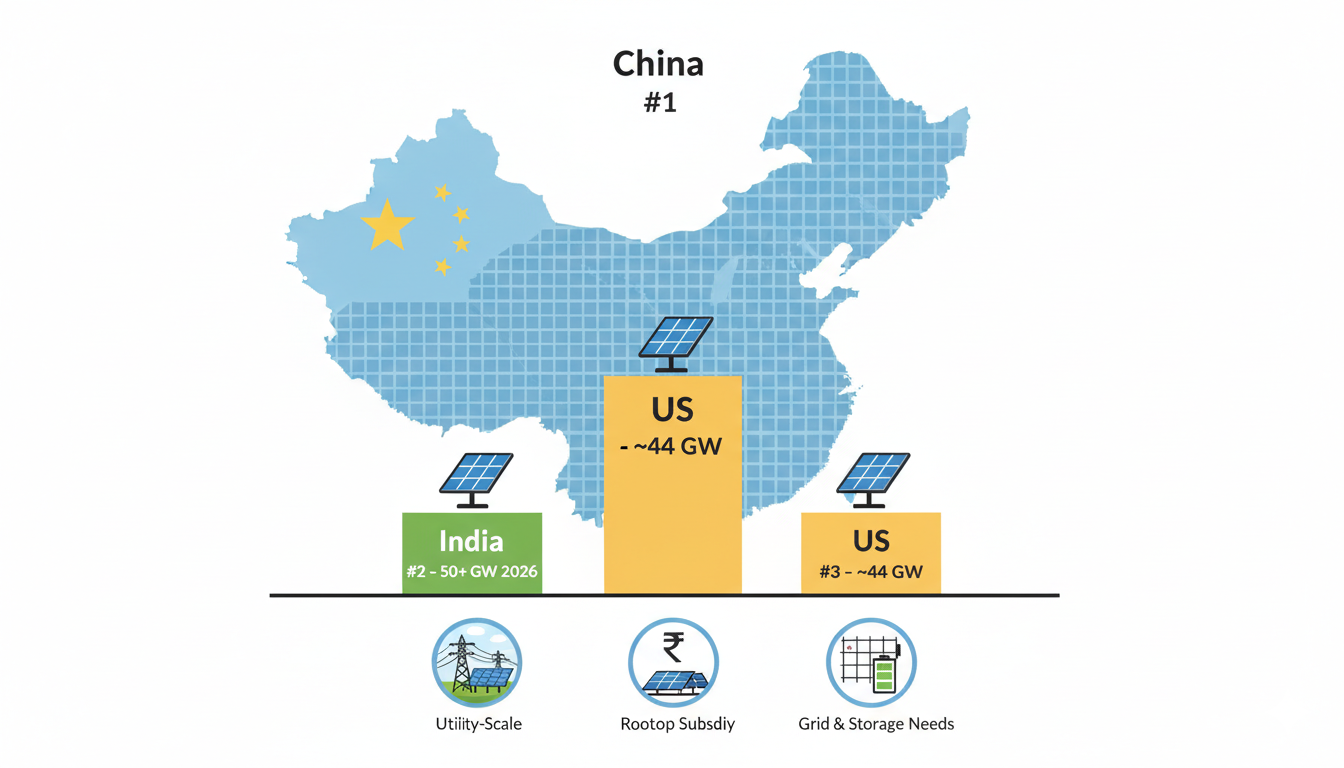

Analysts expect India’s solar additions in 2026 to rise about 6 percent year‑on‑year to slightly above 50 GW, driven mainly by utility‑scale projects and supported by rooftop growth through subsidy programmes like PM Surya Ghar. In the same year, US installations are forecast to fall roughly 14 percent to around 44 GW because of new policy hurdles and “foreign entity of concern” rules affecting tax credits, allowing India to move into the number‑two spot.

This builds on record momentum: India installed about 35 GW of solar in the first 11 months of 2025, firmly aligning with its broader goal of 500 GW of non‑fossil fuel capacity by 2030. Global outlooks already ranked India as the third‑largest solar market in 2024 with around 30.7 GW of additions, after China and the US, so the 2026 jump consolidates a rapid climb in just a few years.

Why India Is Growing While Others Slow

Several factors explain why India’s solar market is expanding even as global additions are expected to plateau or decline slightly in 2026. Ongoing large‑scale tenders and strong pipelines for utility projects from entities like NTPC, SECI and state agencies are keeping utility‑scale capacity flowing.

Government subsidy schemes, including PM Surya Ghar for residential rooftops, help sustain demand from households despite rising module and balance‑of‑system costs. Clear 2030 targets and political prioritisation of energy security and clean‑energy investment give developers and financiers confidence to build multi‑year project plans.

In contrast, the US faces policy uncertainties and new trade‑linked rules that temporarily slow project execution, while China’s market is shifting from explosive growth to a more moderated phase, reshaping global rankings.

Implications for India’s Solar Industry

Becoming the second‑largest solar market makes India a central player in global clean‑energy investment flows and supply chains. Forecasts highlight that India will be the only major market expected to grow in 2026 while global installations decline slightly, which strengthens its bargaining power with manufacturers and financiers.

It also puts pressure on India to accelerate grid upgrades, storage deployment, and domestic manufacturing capacities so that rapid annual additions remain reliable and sustainable rather than creating bottlenecks.

FAQs

Q1. What exactly changes in 2026 for India’s solar ranking?

India is expected to overtake the US and become the world’s second‑largest solar market by annual additions, with just over 50 GW of new capacity.

Q2. How big is the drop in US solar compared to India’s growth?

US installations are forecast to fall about 14 percent to around 44 GW in 2026, while India grows around 6 percent to slightly above 50 GW.

Q3. What drives India’s 50+ GW solar additions in 2026?

The main drivers are strong utility‑scale project pipelines and continued support for rooftop installations through government subsidy schemes.

Q4. How does this help India’s 2030 energy targets?

Record additions in 2025 and 2026 keep India on track toward its 500 GW non‑fossil capacity goal and solidify solar as a core part of the power mix.

Q5. What challenges come with being the #2 solar market?

India must address grid integration, storage, land and approval bottlenecks, and ensure domestic manufacturing can support sustained annual additions.