China, India, and Europe are all expanding solar fast in 2026, but with very different dynamics: China remains dominant, India is the only major market still accelerating, and Europe is entering a more mature but still large growth phase.

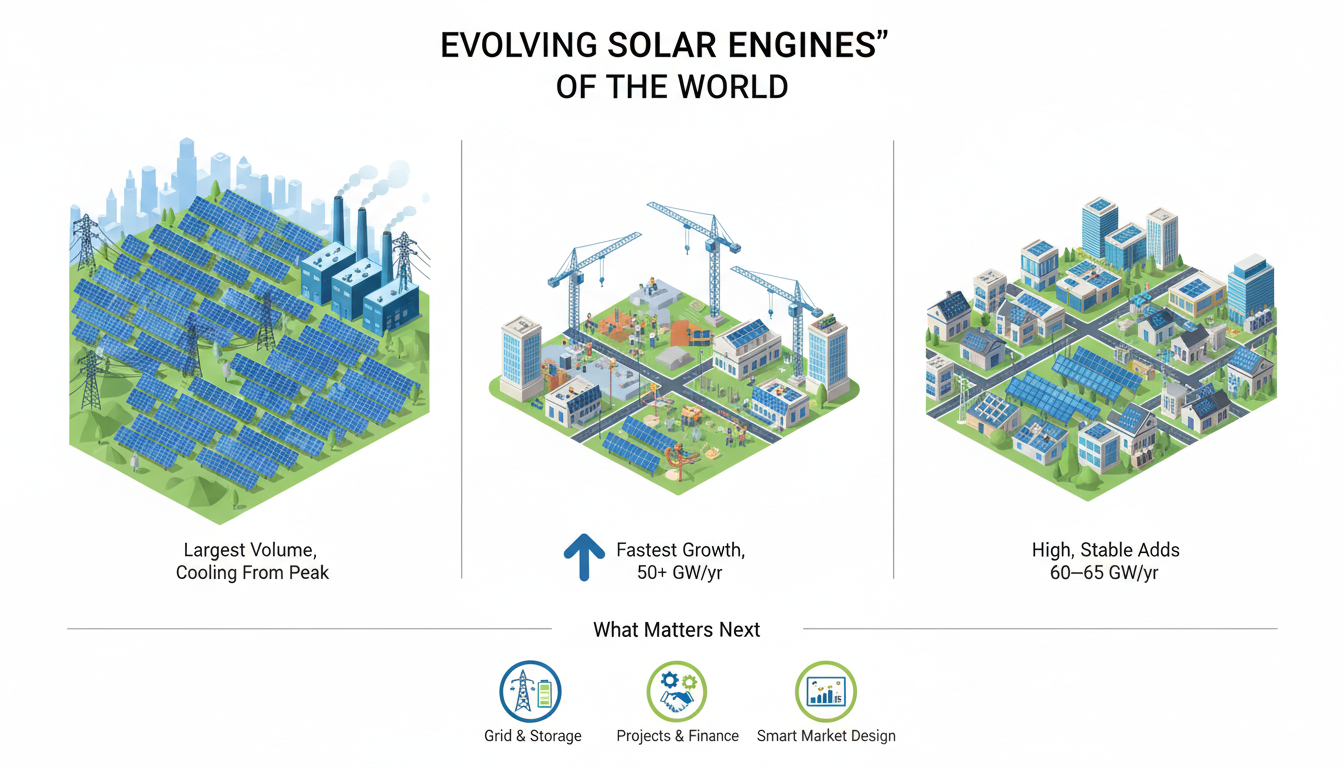

China: Still #1, But Cooling from Record Highs

Forecasts for 2026 suggest China will again be the largest solar market by a wide margin, with BloombergNEF projecting around 321–341 GW of new capacity in 2026, even after a planned slowdown from an estimated 372 GW in 2025. Policy changes—especially a new market‑based pricing mechanism and grid‑integration constraints—are expected to moderate the “breakneck” pace, but China will still account for roughly half of global additions in 2026.

India: Fastest Growth Among Major Markets

India is the standout mover in 2026, expected to overtake the US and become the world’s second‑largest solar market by annual additions. BloombergNEF and other outlooks indicate India will add just over 50 GW of solar in 2026—about 6 percent more than in 2025—while the US drops to around 44 GW because of new regulatory hurdles. Global Market Outlook data also shows India rising from about 30.7 GW additions in 2024 into a sustained high‑growth trajectory through 2029, supporting its 500 GW non‑fossil capacity target for 2030.

Europe: Large but Flattening After a Surge

The EU saw a huge build‑out in 2022–2025, with annual installations rising toward the mid‑60 GW range and total capacity expected to reach around 484 GW by 2026 under earlier scenarios. Recent updates, however, show EU solar additions at about 65.1 GW in 2025, the first slight year‑on‑year drop after a decade of growth, and projections suggest a flatter curve from 2026 as markets digest rapid recent expansion and grid and permitting issues are addressed. Even with this moderation, Europe remains one of the three largest regional solar markets and is expected to keep adding tens of GW per year through 2030, driven by energy‑security goals and rooftop adoption.

Global Picture for 2026: Slight Slowdown, Strong Non‑China Growth

SolarPower Europe’s Global Market Outlook projects global additions around 655 GW in 2025 and roughly 665 GW in 2026 under its “most likely” scenario, implying only about 1 percent growth in 2026. BloombergNEF’s updated view is even more cautious, seeing a small year‑on‑year dip in 2026 (around 649 GW vs. 655 GW) as China’s growth cools, even though solar deployments outside China are projected to exceed 300 GW for the first time. In other words, non‑China markets—led by India, parts of Europe, Latin America, and Southeast Asia—continue to grow, but not enough to fully offset China’s deliberate slowdown.

What This Means for Developers and Policymakers

By 2026, the “fastest expansion” story is less about absolute volume (where China still dominates) and more about relative growth and market rebalancing: India is the key growth engine, Europe is stabilising at a high level, and China is shifting from pure volume toward market design, grid integration, and storage. For policymakers and companies, this means success depends less on chasing raw GW numbers and more on execution—securing grid capacity, batteries, flexible demand, and strong EPC/financing partnerships to make large annual additions actually deliver reliable, usable power.

FAQs

Q1. Which country will add the most solar in 2026?

China will remain number one, with about 320–340 GW of new solar capacity expected in 2026, roughly half of global installations.

Q2. Which major market is growing fastest in percentage terms?

India is projected to grow solar additions by about 6 percent to just over 50 GW in 2026 and overtake the US as the second‑largest market.

Q3. Is global solar still growing in 2026?

Forecasts show global additions roughly flat or slightly down around 649–665 GW in 2026, as China slows but non‑China markets keep rising.

Q4. How is Europe’s solar market performing around 2026?

The EU is expected to stay a top region with around 60–65 GW a year, but 2025 already showed a small dip after a decade of continuous growth.

Q5. What is the main structural shift in 2026’s solar boom?

The focus is shifting from raw capacity growth to integration—grid upgrades, storage, and smarter market design—especially as China cools and India and Europe carry more of the incremental growth.