China is on track to dominate global solar growth this decade, with solar capacity and clean‑energy investment expanding at a pace no other country currently matches. Analysts expect China to contribute well over half of the world’s new renewable capacity by 2030, driven largely by solar manufacturing and deployment.

China’s Solar Surge: Scale and Speed

China added about 277–278 GW of new solar capacity in 2024 alone, a roughly 28 percent year‑on‑year increase that pushed its total solar capacity close to 900 GW by the end of that year. Clean‑energy investment has grown roughly ten‑fold in five years, and solar now accounts for the majority of new zero‑emission power additions in China. By 2030, the IEA projects that China will account for more than half of global renewable capacity, with solar leading this expansion.

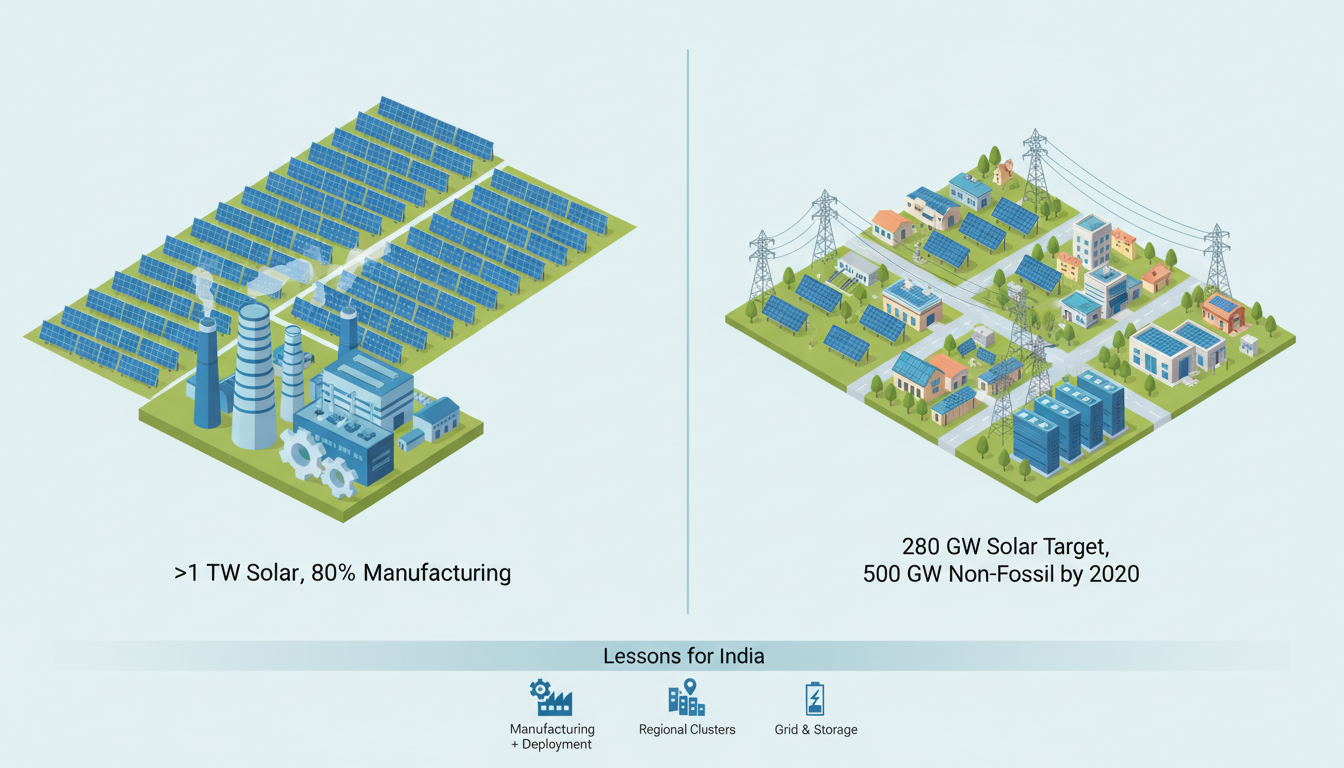

This acceleration allowed China to meet its 2030 target of 1.2 TW of wind and solar capacity several years ahead of schedule and to set its sights on 3,000 GW of renewables by 2030. In mid‑2025, China crossed the symbolic 1 TW mark in solar alone, nearly ten times India’s installed solar capacity at that point.

What Enabled China’s Leadership?

Several structural choices explain why China’s solar growth looks so steep compared to the rest of the world. Full‑stack manufacturing dominance means China produces more than 80 percent of the world’s solar PV modules and leads across wafers, cells, and panels, creating strong cost and supply‑chain advantages.

Policy continuity and scale through clear multi‑year targets in five‑year plans, utility‑scale “Top Runner” programmes, and grid‑planning integrated with renewable expansion have aligned central and provincial priorities. Massive, predictable demand from large solar parks and distributed rooftop programmes created sustained internal demand, while infrastructure and land readiness via earmarked land, transmission corridors, and industrial zones cut project timelines and soft costs.

The result is an ecosystem where policy, industry, finance, and grid operators move in the same direction, reducing friction at every stage from manufacturing to grid connection.

India’s Position: Strong Progress, Different Constraints

India has also moved quickly, reaching around half its installed power capacity from non‑fossil sources years ahead of its 2030 target and pushing toward 500 GW of non‑fossil capacity by 2030, largely on the back of solar. India’s solar capacity has been expanding, and manufacturing is ramping up under schemes like PLI and the Approved List of Models and Manufacturers (ALMM), which aim to build 70+ GW of annual cell and module capacity and close much of the investment cost gap with China.

However, India still faces fragmented state policies, slower land acquisition, grid constraints, and under‑utilised module factories, some of which operate at only about a quarter of capacity due to demand and policy bottlenecks. The challenge is less about ambition and more about scaling execution infrastructure, grid readiness, and manufacturing competitiveness in a coordinated way.

Key Lessons India Can Draw from China’s Solar Push

India does not need to copy China, but several lessons are directly relevant to India’s 2026–2030 roadmap. One is to treat manufacturing and deployment as one system, aligning incentives so that domestic manufacturing, project development, and grid upgrades evolve together, instead of in isolated silos.

India can also build regional clean‑energy clusters, not just individual projects, deepening hubs where manufacturing, testing labs, logistics, and large projects sit together. Cutting soft costs with streamlined approvals and land policy, investing early in grid flexibility and storage, and focusing on technology depth—not just volume—are further lessons drawn from China’s experience.

What This Means for Indian Policy and Industry 2026–2030

For India, the real global lesson is that solar leadership is built on consistent policy, long‑term manufacturing bets, and grid‑level thinking rather than on annual tender volumes alone. If India combines its ambitious 280 GW solar target for 2030 with smoother approvals, stronger domestic manufacturing, and early storage investments, it can narrow the execution gap with China while building a more diversified, resilient ecosystem.

FAQs

Q1. How fast is China’s solar capacity growing compared to the world?

China added around 277–278 GW of solar in 2024 alone and has accounted for over half of global solar additions in recent years.

Q2. What is China’s solar milestone that India is compared against?

China passed 1 TW of installed solar capacity in 2025, roughly ten times India’s solar capacity at that time.

Q3. What is India’s solar target for 2030?

India targets around 280 GW of solar within a broader 500 GW non‑fossil capacity goal by 2030.

Q4. What is the biggest structural difference between China and India in solar?

China has a deeply integrated manufacturing‑to‑deployment ecosystem, while India still faces fragmented policies, land and grid bottlenecks, and under‑utilised factories.

Q5. What should India prioritise from 2026–2030 to learn from China?

India should prioritise manufacturing‑deployment integration, regional clean‑energy clusters, streamlined clearances, storage and grid upgrades, and targeted R&D in advanced solar technologies.