China is setting unprecedented records in renewables, with solar at the core of its growth story. In 2024, China alone added around 329 GW of solar—about 55 percent of all new solar installed worldwide that year—and is now responsible for the majority of global solar expansion. By 2025, its combined wind and solar additions were about 360 GW, pushing total capacity for these technologies to roughly 1.4 TW, the largest in the world by far.

China’s Record-Breaking Solar Buildout

Recent analyses show that in the first half of 2025, global solar installations hit a record 380 GW, with China contributing about 256 GW—roughly two‑thirds of the world’s new capacity in that period. Earlier data from S&P Global and SolarPower Europe highlight that China added about 277–329 GW of solar in 2024 alone, accounting for most of the global market’s net new PV capacity. In some 2025 months, China was installing solar at the equivalent of nearly 100 panels per second, underscoring the sheer speed and industrial scale of its rollout.

This surge means China’s installed solar PV capacity has crossed 1 TW and now represents roughly half of global solar capacity, firmly establishing it as the central driver of renewable expansion. Clean energy (including solar, wind, batteries, and related technologies) is estimated to contribute around 10 percent of China’s GDP, signalling how deeply renewables are now woven into its economic strategy.

Why China’s Expansion Matters for the Global Market

China’s dominance affects global renewables in three main ways: it drives down module and component prices through economies of scale and intense competition, influencing project economics everywhere, including India; it concentrates much of the PV manufacturing supply chain in one country, raising concerns about over‑reliance and prompting “China plus one” diversification strategies; and it accelerates global emissions reductions by shifting a large power system away from coal, but also raises integration challenges—curtailment, grid stress, and local overcapacity—that other countries can learn from.

Global reports note that while China’s buildout has helped push solar to become the fastest‑growing source of new electricity generation, it has also led to concerns about over‑investment and regional grid bottlenecks inside China.

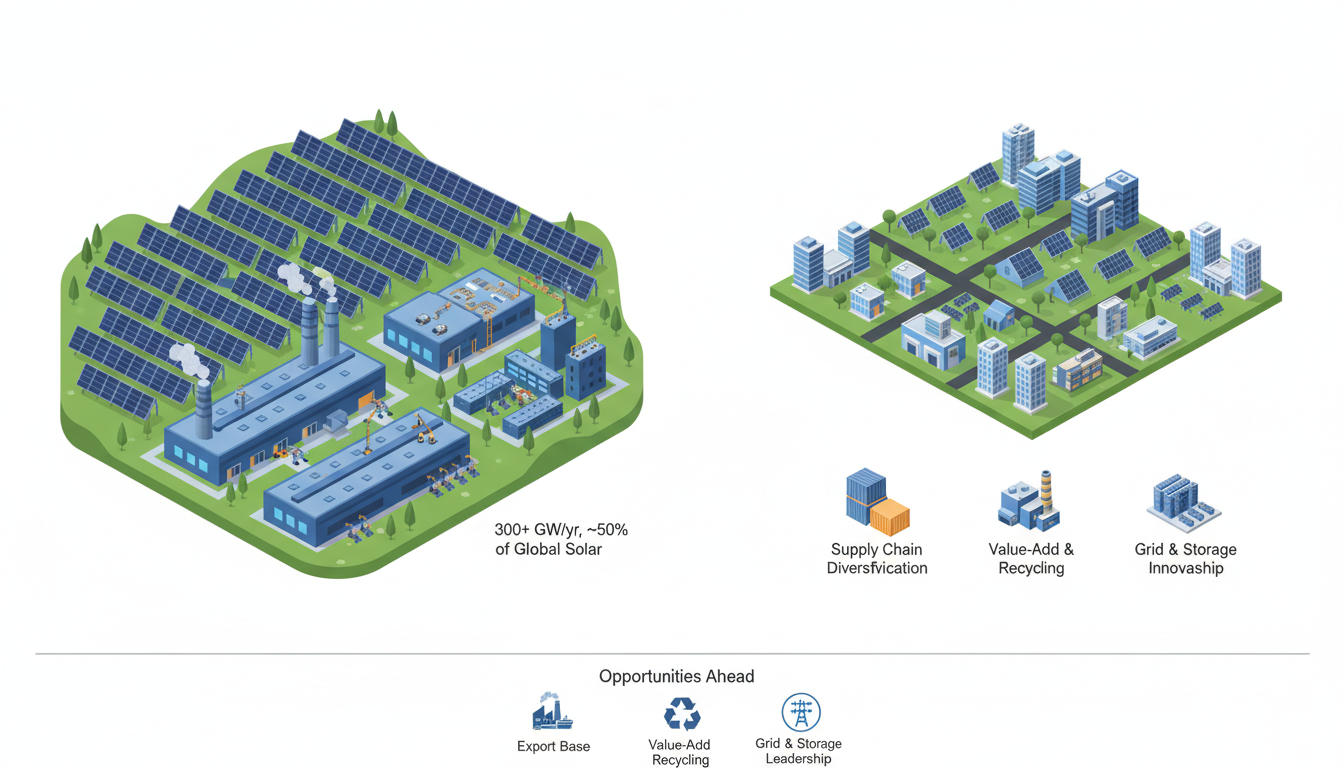

Strategic Opportunities for India from China’s Leadership

“China Plus One” Supply Chain Positioning

As governments and companies seek to de‑risk supply chains and avoid single‑country dependence, India is emerging as a preferred alternative manufacturing base. Analyses suggest India can expand its role in modules, selected upstream components, and especially in export‑oriented production for markets implementing diversification policies, such as the US and parts of Europe.

Targeted Value-Chain Niches

Expert reviews recommend that India focus on specific segments where it has comparative advantages: high‑quality module assembly, BOS components (structures, cables, inverters integration), and eventually PV recycling and circular‑economy services as the first global wave of panels reaches end of life. Entering recycling early could reduce long‑term raw‑material dependencies and create a differentiated, high‑value services industry around spent modules and batteries.

Leveraging Cheaper Hardware for Faster Domestic Deployment

China’s scale has helped lower module prices globally, which India can leverage to accelerate its own deployment, especially in utility‑scale parks and distributed rooftop under schemes like PM Surya Ghar. Reports emphasise that India remains a net importer of Chinese modules today but can use current low prices to quickly build capacity while simultaneously nurturing domestic manufacturing under PLI and related schemes.

Learning from China’s Grid and Storage Experience

China’s rapid build has forced it to innovate in grid integration—through batteries, pumped hydro, virtual power plants, and flexible demand—after facing curtailment and overcapacity in some regions. India can adopt and adapt these approaches early, building storage and grid‑flexibility into its expansion plans so that very high annual additions (50+ GW) remain usable and financially viable.

Deepening International Clean-Energy Partnerships

India’s diplomatic work—particularly through the G20 and International Solar Alliance—is already framing the country as a central hub for diversified clean‑energy supply chains. As investors look for alternatives to purely China‑centric value chains, India can attract more climate finance by offering stable demand, policy support, and localisation pathways for components and services.

FAQs

Q1. What does “390+ GW solar records” refer to in China’s case?

Various 2024–2025 assessments show China adding on the order of 300+ GW of solar in a single year and around 256 GW in just the first half of 2025, plus large wind additions, pushing combined new renewables toward the 360–390 GW range.

Q2. How dominant is China in new global solar installations?

In the first half of 2025, China installed about 256 GW of solar—around 67 percent of global additions—while the rest of the world combined added roughly 124 GW.

Q3. Where does India stand relative to China today?

India was the second‑largest solar market by additions in H1 2025 with 24 GW, far behind China’s 256 GW but ahead of the US, which installed about 21 GW.

Q4. Why is the world trying a “China Plus One” strategy in solar?

Heavy dependence on China for PV manufacturing, combined with trade tensions and supply‑chain shocks, has pushed countries and firms to diversify production into places like India, Vietnam, and Mexico.

Q5. How can India benefit most from China’s renewable leadership?

By using low global hardware prices to speed domestic deployment, building competitive manufacturing in chosen value‑chain segments, investing early in recycling and storage, and positioning itself as a diversified, reliable clean‑energy hub.